The National Electricity Market

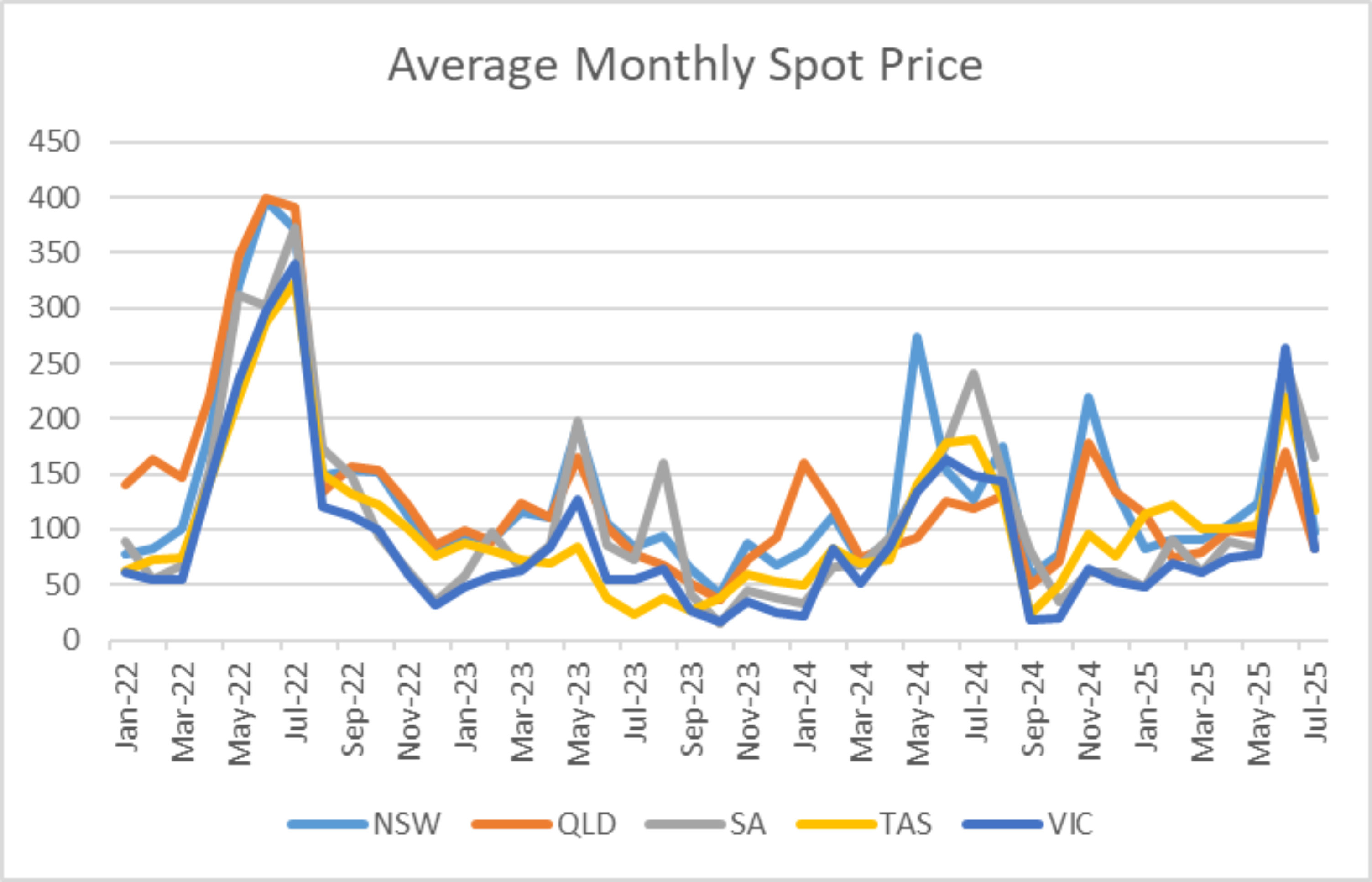

Wholesale electricity prices in July returned to “normal” after the spike experienced last month due to high volatility across the NEM. Average prices decreased in all States ranging from 34% in SA up to 69% in VIC. Average prices ranged from the low $80s in QLD and VIC up to $165 in SA.

Electricity Generation Mix

Total grid-scale generation for July increased by 3.6% from June levels – relatively unchanged in operational demand given there is one more day in July.

Solar and Wind generation increased significantly while Gas and Hydro had large falls compared to the previous month.

Gas Generation

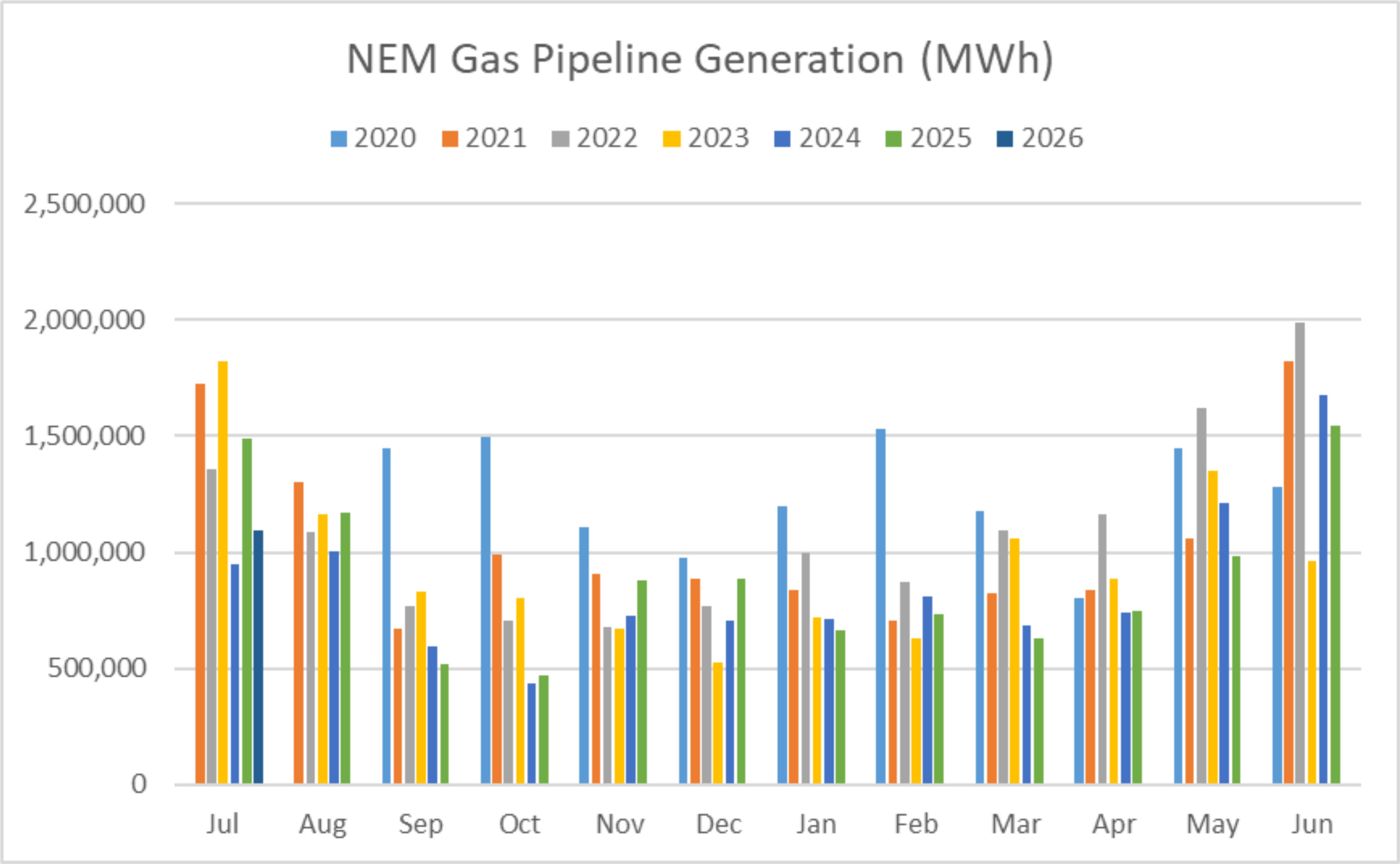

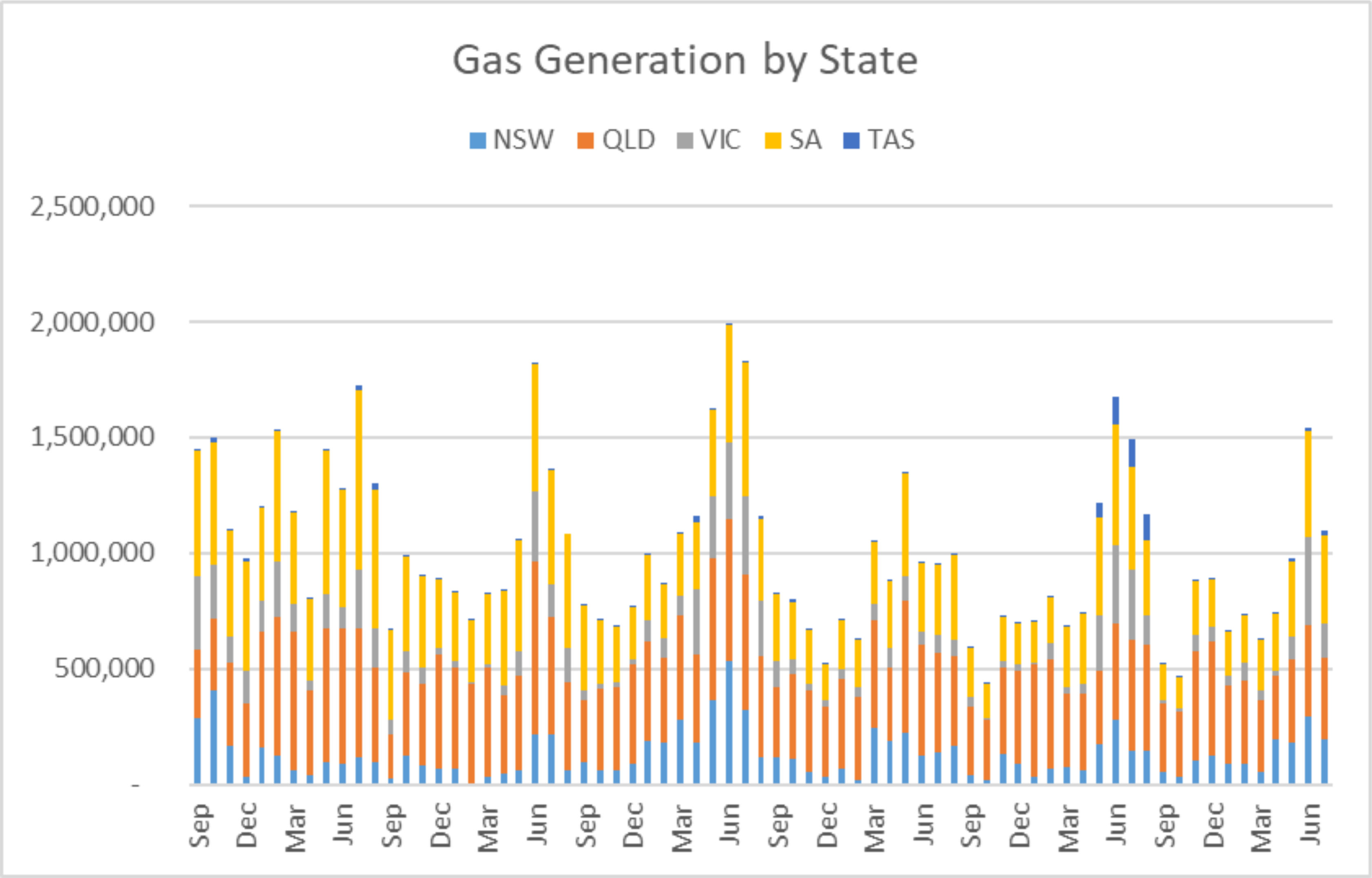

Gas generation decreased significantly in July – down 29% compared to June. Compared to 12 months ago gas generation was 27% lower than it was in July 2024.

Gas generation was down in all States but particularly VIC which decreased 62%. NSW fell 33%, TAS 21%, SA 15%, and QLD 11%.

Hydro Generation

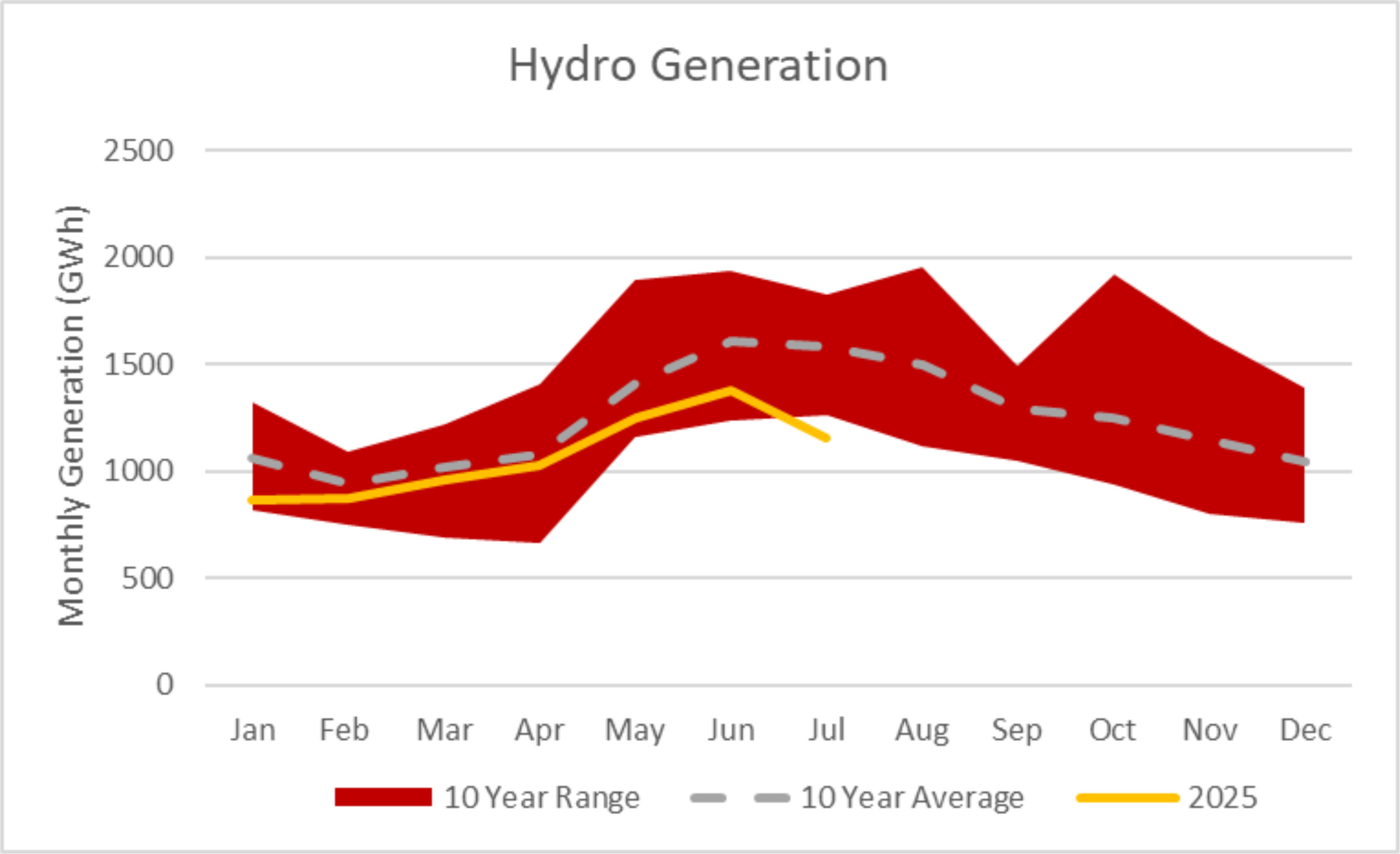

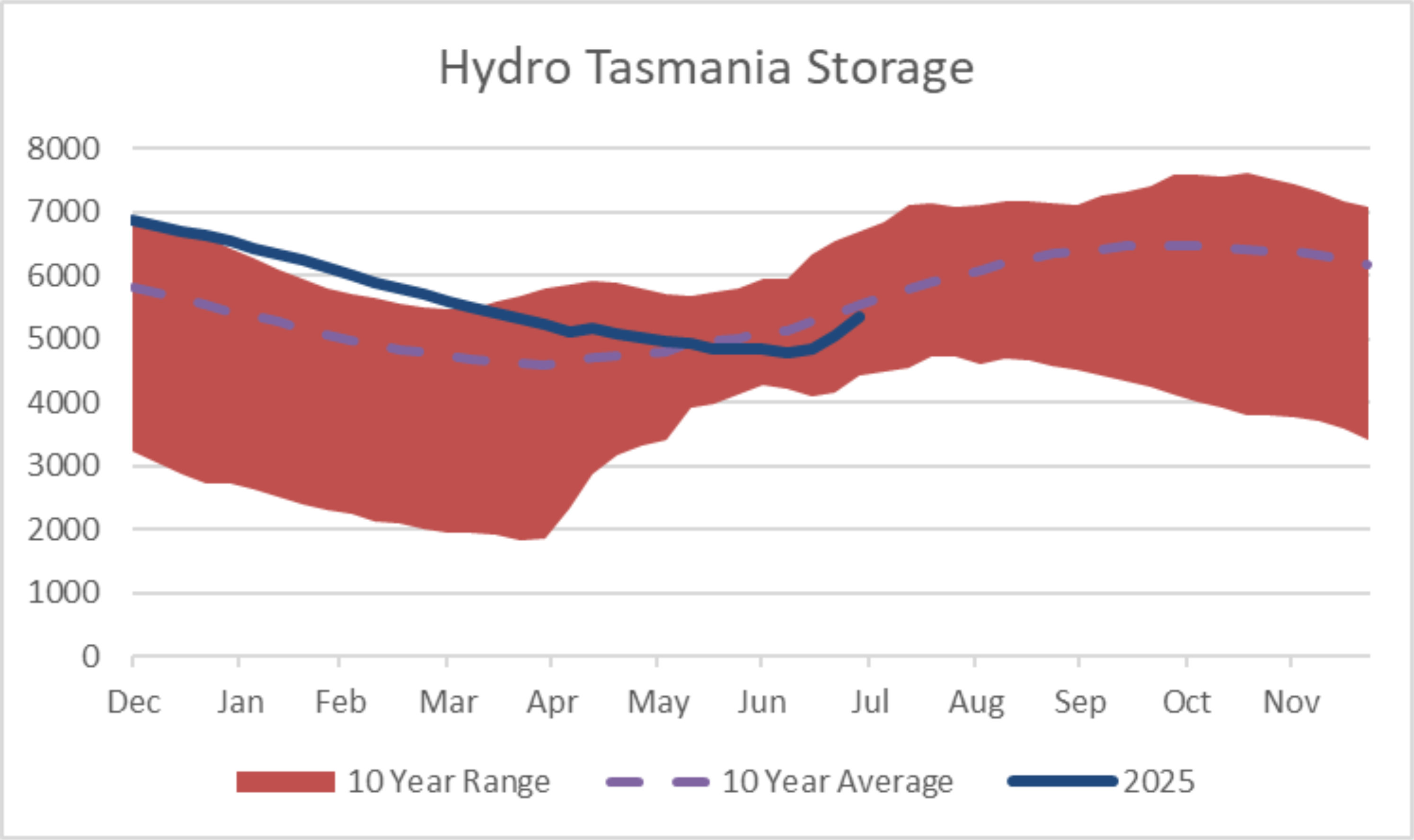

Hydro generation decreased 16% in July compared to June levels, dropping below its lowest level seen in the last 10-years, for this time of year, as shown below.

Storage in Hydro Tasmania’s lakes increased markedly in July. Storage ended the month at 5,354GWh (37% full), an increase of 500GWh over the month. This is 8% more than the same time last year and back close to the average level seen at this time of year in the last 10 years, as shown in the following chart.

Snowy Hydro’s storage increased for the first time since late 2024. Snowy finished the month 37% of full (1,982Gl) – a 6% increase over the month. Levels remain well below the 10-year average for this time of year as shown in the following chart.

Climate outlook overview (from BOM)

The long-range forecast for August to October shows:

- Rainfall is likely to be above average for most of mainland Australia.

- Warmer than average days are likely across northern, western and south-eastern Australia, with an increased chance of unusually high daytime temperatures in the far north and across Tasmania.

- Warmer than average nights are likely to very likely across Australia, with an increased chance of unusually high overnight temperatures for northern, eastern and central Australia.

New Renewable Generation (Excluding Hydro)

Total renewable generation (wind and solar, including roof-top solar) in July was 6,480GWh – up 20% from last month’s level, and up 21% on the same month last year. Wind generation hit a new record high of 3,743GWh for the month eclipsing the previous record from June 2023 by more than 20%. Utility Scale Solar generation was up 10% from June’s levels and 17% over the same month last year.

The following chart shows the monthly energy produced for each of these renewable types since 2017.

The Electricity Futures Market

Futures prices drifted lower through July in most States, across every calendar year.

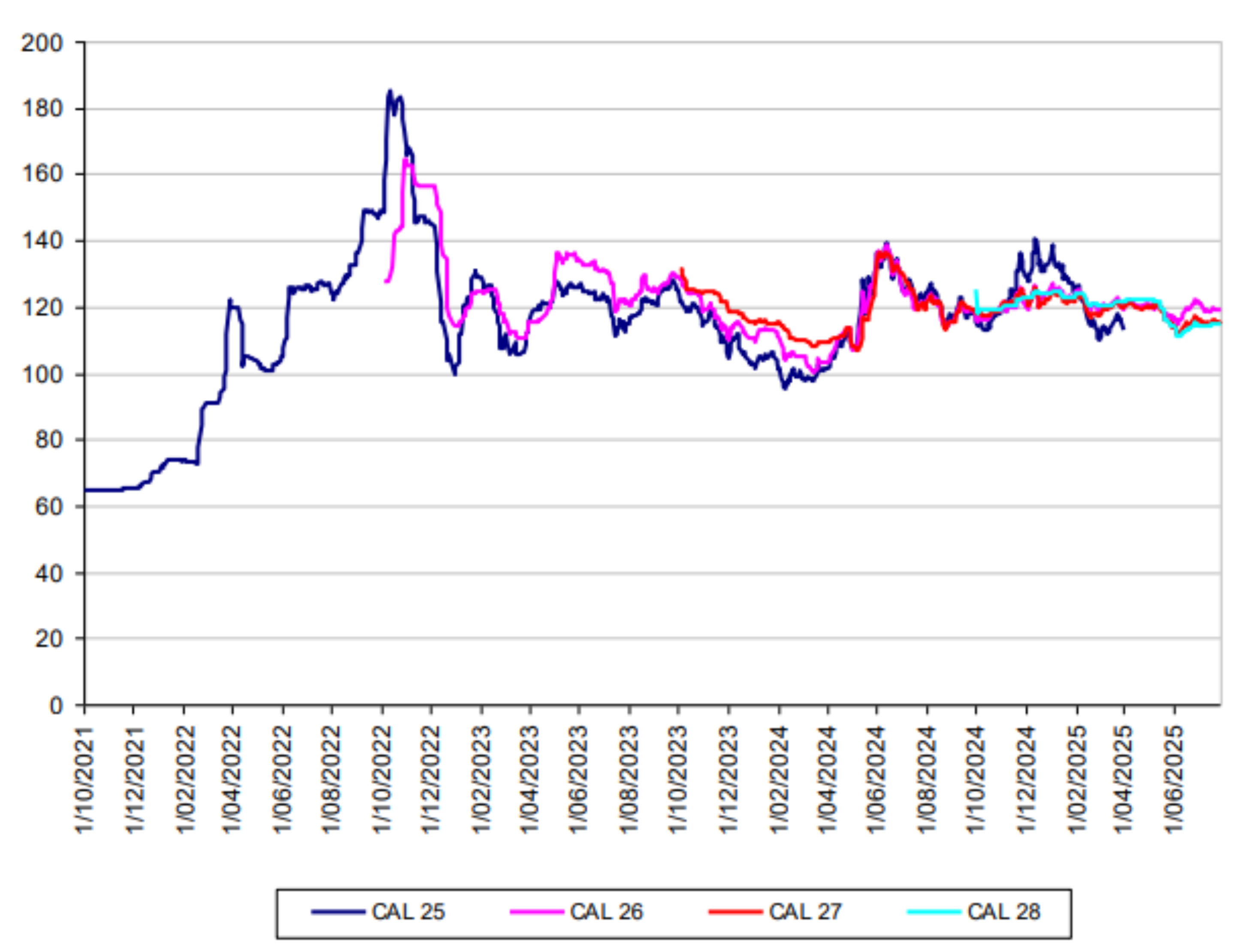

In NSW CAL26 was down 2% at $119, while CAL27 was down 1% ($115) and CAL28 unchanged ($115).

Calendar Year Contracts for New South Wales

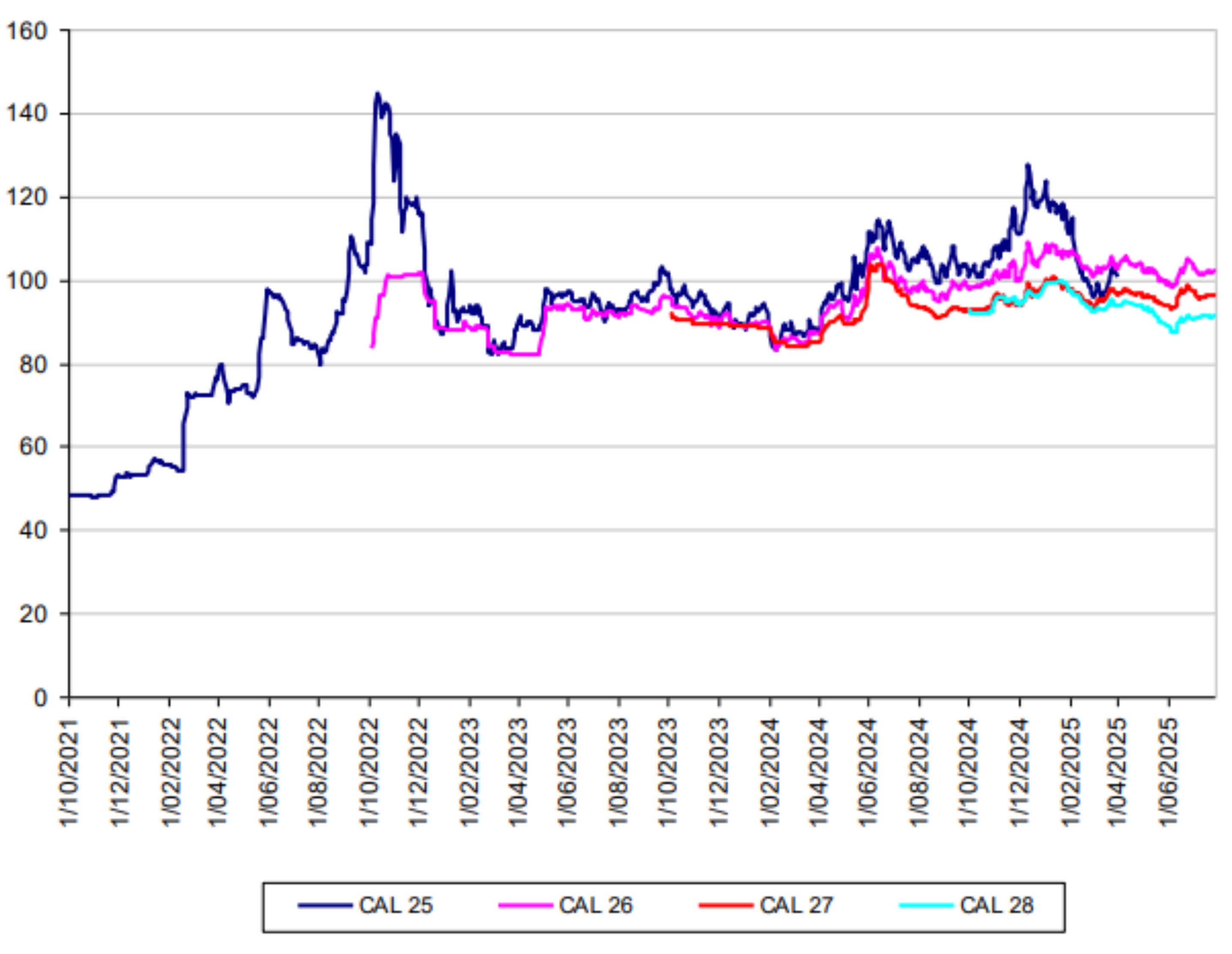

QLD prices followed a similar pattern to NSW. CY 2026 was down 2% at $102. CAL27 was down 1% ($96) and CAL 28 was flat ($91).

Calendar Year Contracts for Queensland

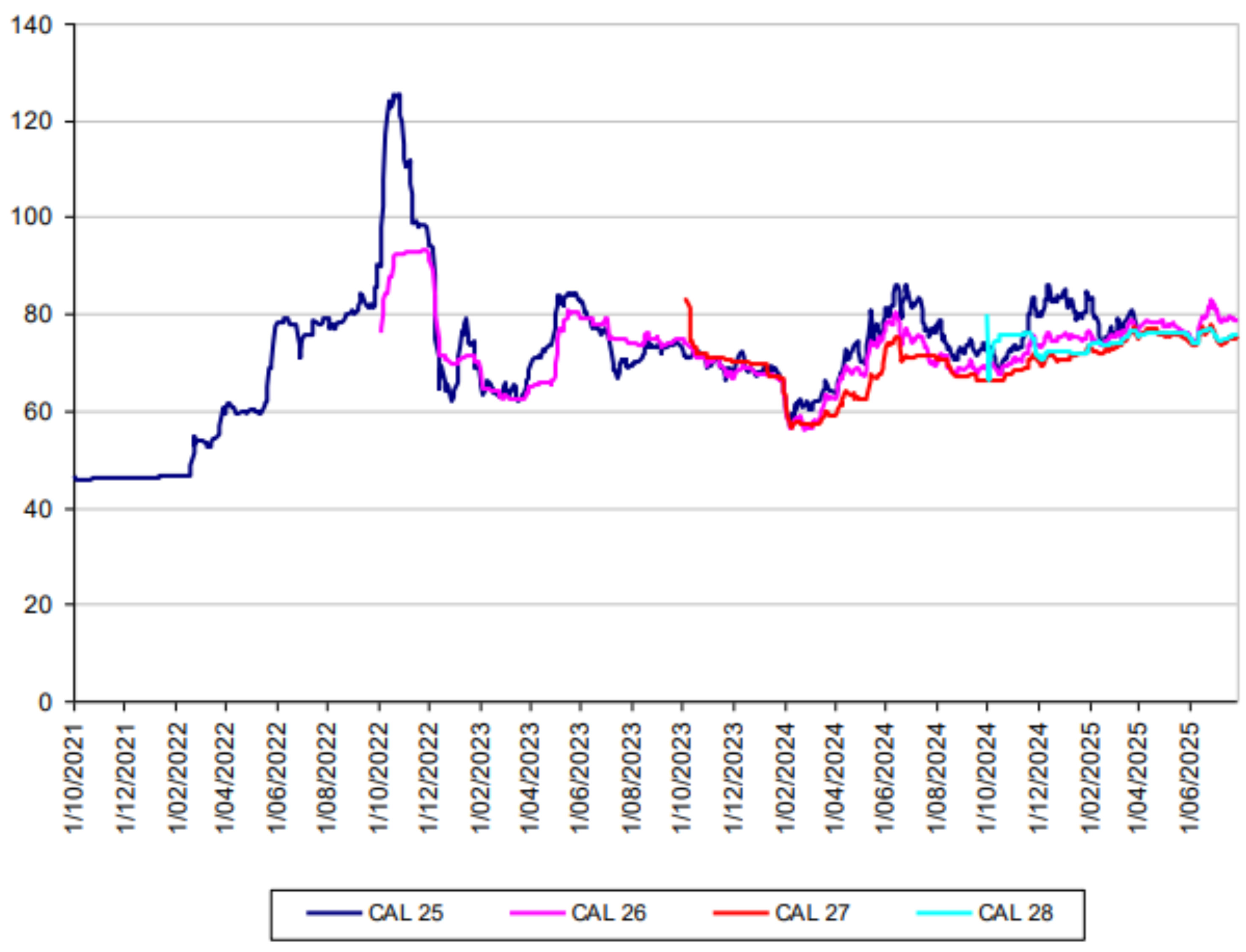

VIC futures prices for CAL26 were down 4% at $77, CAL27 was down 1% at $75, while CAL28 was unchanged at $76.

Calendar Year Contracts for Victoria

SA has less liquidity in the futures markets than other States, so changes tend to be lumpier and less a true reflection of the underlying market. For completeness we have included the graph below.

Calendar Year Contracts for South Australia

The Gas Market

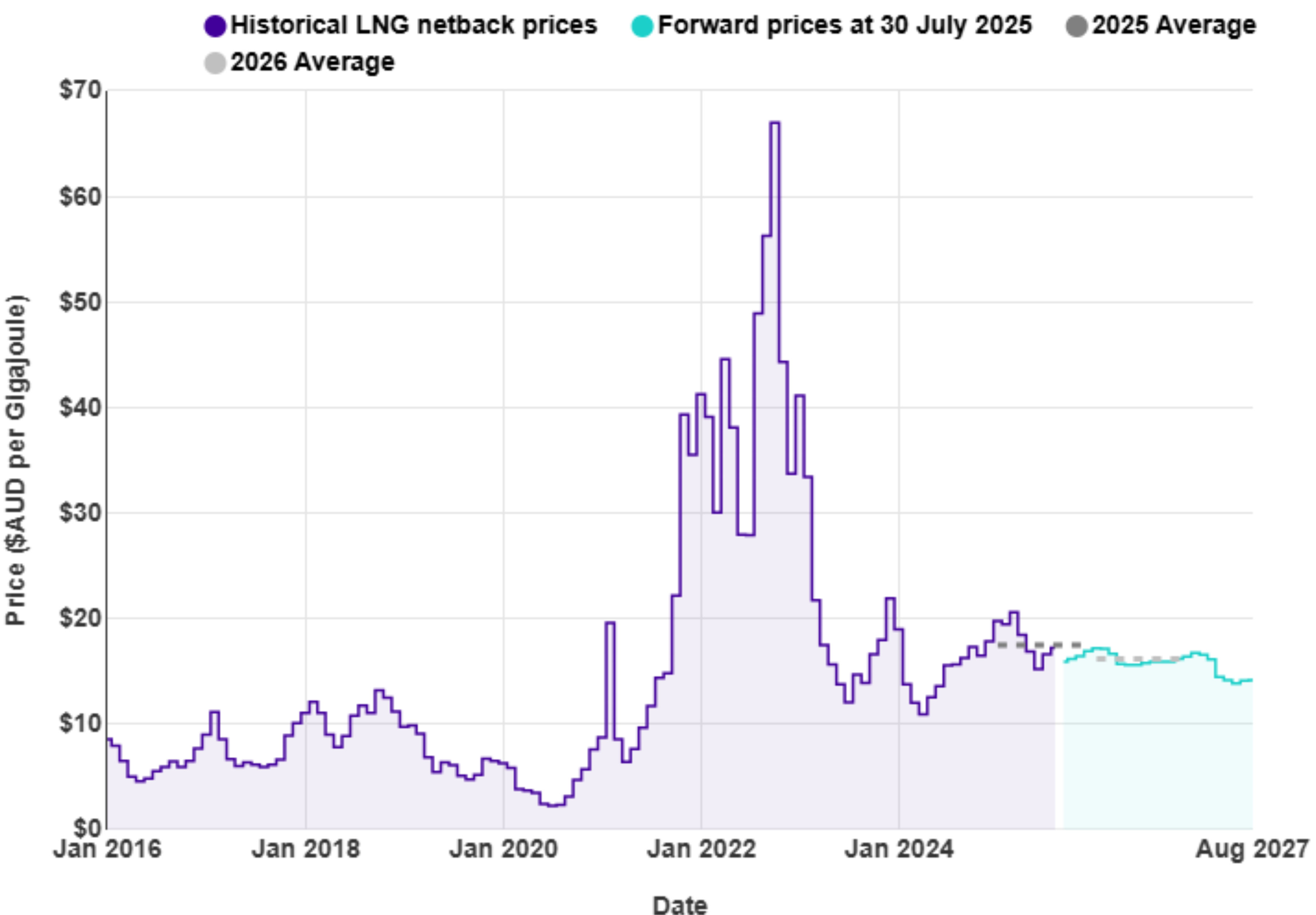

Internationally, LNG netback prices ended the month at $17.23/GJ – up 4% from last month. Forecast prices for 2025 were flat at $17.48/GJ. Forward prices for 2026 were also flat at $16.18/GJ. (Note that netback prices are indicative of international prices – they are produced by the ACCC and quoted in Australian dollars. They are net of the estimated costs to convert from pipeline gas in Australia to LNG, hence the term “netback”)

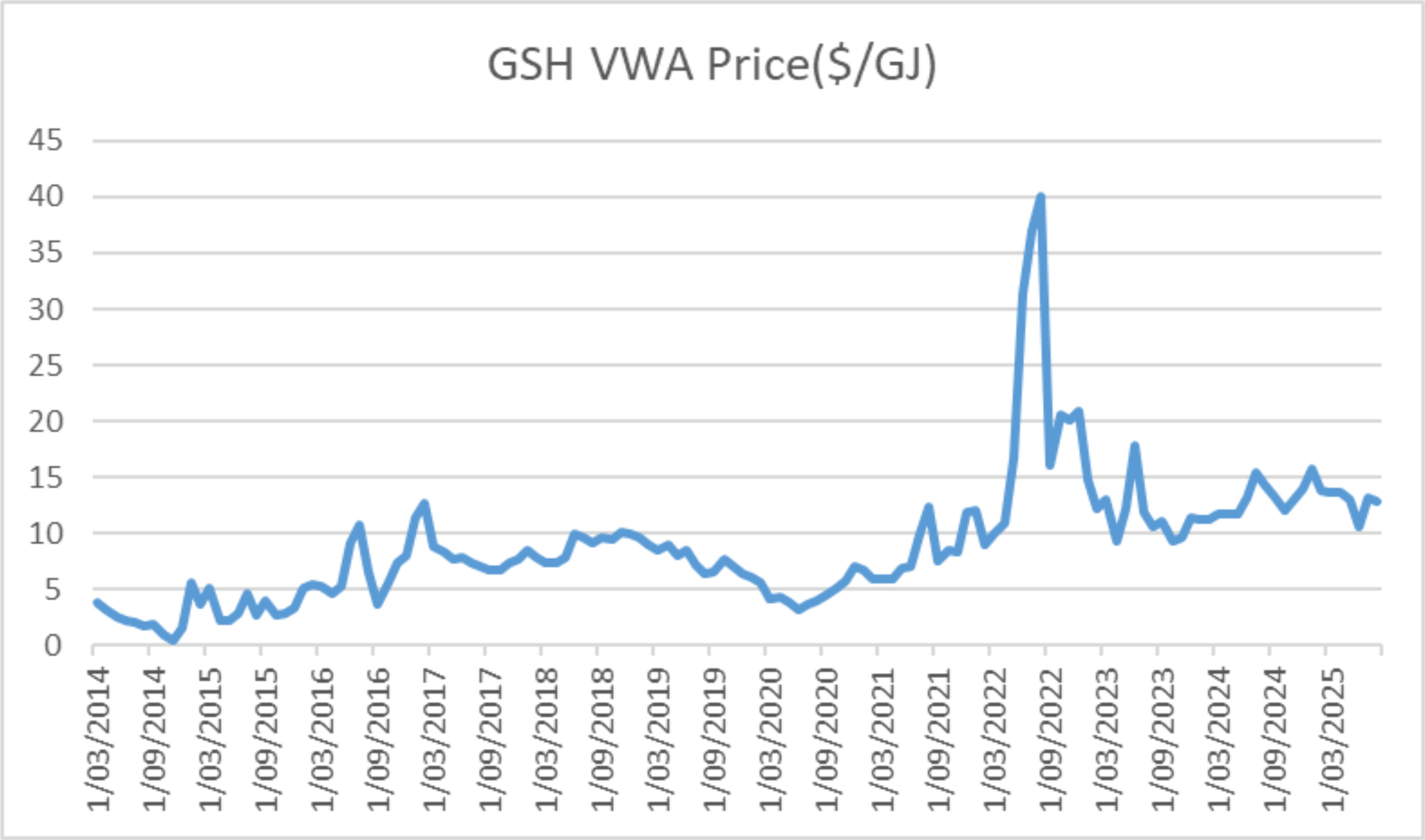

Domestic spot gas prices dropped slightly in July. The following graph shows the 30-day rolling average price at Wallumbilla gas supply hub – ending the month at $12.8/GJ, down 2.6% from June levels. This is still well below the LNG netback price. Prices are still 10% below what they were the same time last year.

Gas storage at the key Iona storage facility continued to fall through July but at a slower rate than it did in June. Storage decreased to 13PJ – a 22% fall over the month. Storage remains close to the average levels we have seen at this time of year for the past 9 years.

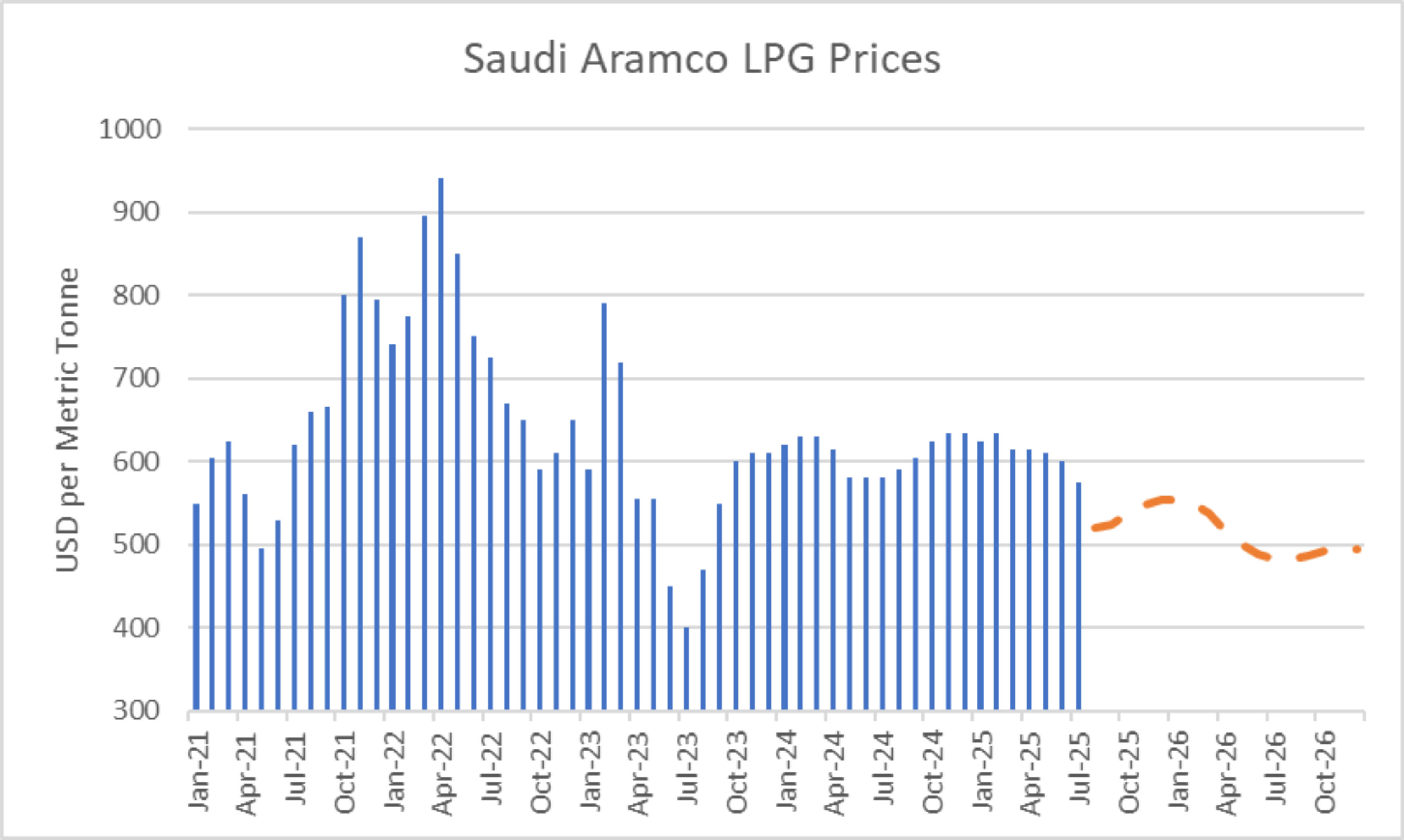

LPG is an important fuel for many large energy users, particularly in areas where reticulated natural gas is not available. The contract price of LPG is typically set by international benchmarks such as the Saudi Aramco LPG price – normally quoted in US$ per metric tonne.

The following graph shows the Saudi Aramco LPG pricing for the last 4.5 years as well as forecast pricing for the year ahead. Futures pricing were down over the last month and remain trending down through 2026.

The other main contributing factor to LPG prices in Australia is the exchange rate against the USD. The exchange rate hovered around 0.65 for much of July, dropping to 0.64 at the end of the month. This remains near the lowest levels seen in recent years. This would tend to push up LPG prices when quoted in AUD.

The Coal Market

The global energy crisis has been as much about coal as it has gas. The war in the Ukraine has driven energy prices, including coal, up. Prices in July increased ending the month at US$115/T – a 5.5% rise over the month. These prices are finally returning to levels close to what we expect to see as shown in the following graph of prices over the last 10 years.

International coal prices continue to be an important driver of electricity prices especially in the States most reliant on black coal generation – ie QLD and NSW.

Environmental Certificates

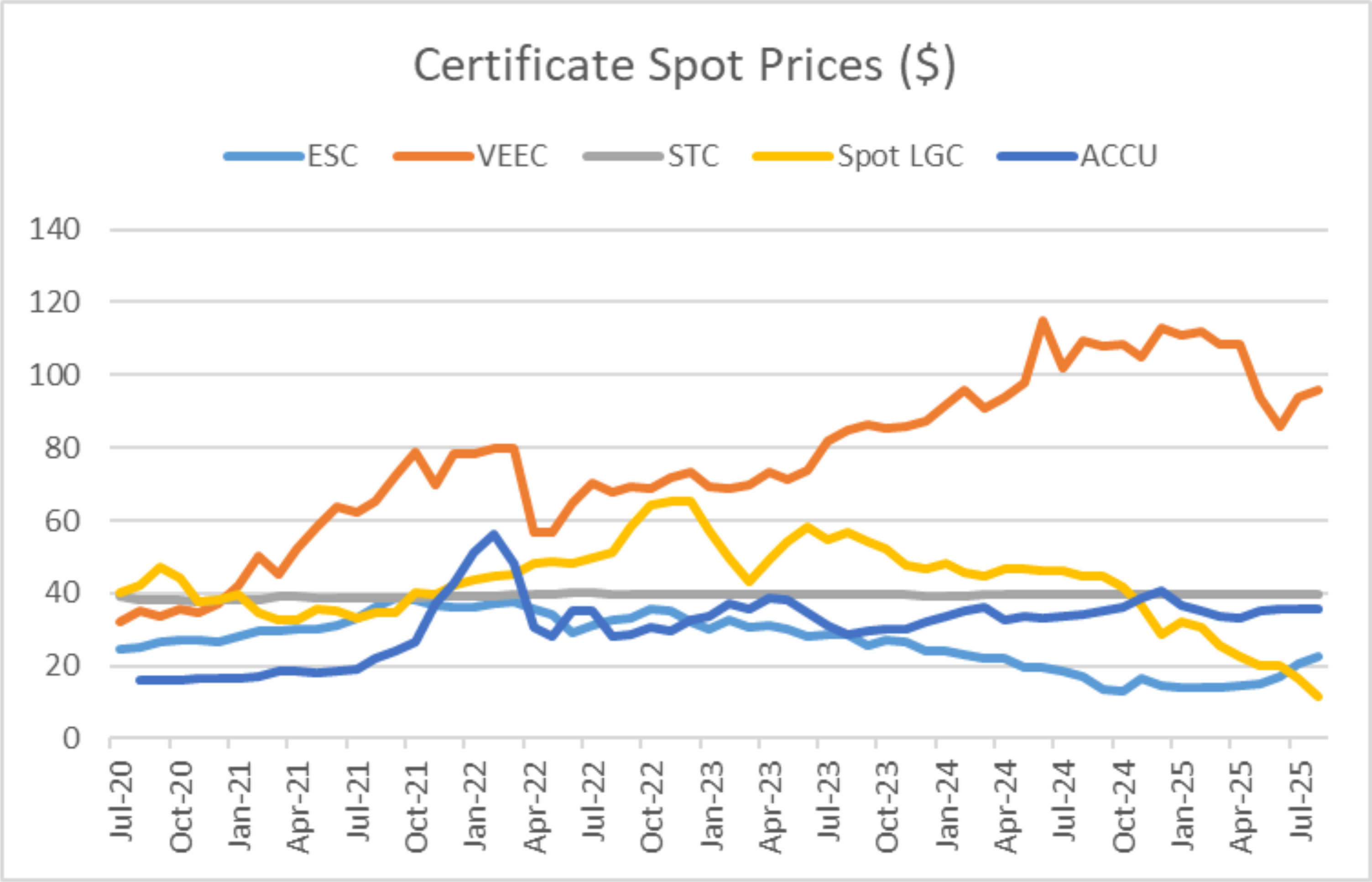

The following graph shows environmental certificate spot prices over the last 5 years.

Spot LGCs continued their steep decline through July, falling a further 32% to $11.3. VEECs, ACCUs and STCs were all relatively unchanged. ESCs continued recent gains, up 10% to $22.25.

Future dated LGC prices accelerated the rate of decline observed over several months. CAL25 was down 26% at $12, while CAL26 decreased by 30% to $11. CAL27 fell by 39% to $8 while CAL28 also dropped 26% to $7.5. CAL29 continued the trend decreasing 24% to $7.

About this Report

This energy market summary report provides information on wholesale price trends for all regions within the National Electricity Market (NEM) and environmental scheme certificates.

Please note that all electricity prices are presented as a $ per MWh price and all certificate prices as a $ per certificate price.

All NEM spot prices are published by the Australian Energy Market Operator (AEMO). Futures contract prices are sourced from ASX.

Further information can be found at the locations noted below.

- NEM Spot market – AEMO publishes a range of detailed information which can be found here: https://aemo.com.au/Electricity/National-Electricity-Market-NEM/Data-dashboard

- Weather and Climate data – The Bureau of Meteorology publishes a range of weather related information which can be found here: http://www.bom.gov.au/climate/

Disclaimer

This document has been prepared for information and explanatory purposes only and is not intended to be relied upon by any person. This document does not form part of any existing or future contract or agreement between us. We make no representation, assurance or guarantee as to the accuracy of information provided. To the maximum extent permitted by law, none of Smart Power Utilities Ltd, its related companies, directors, employees or agents accepts any liability for any loss arising from the use of this document or its contents or otherwise arising out or, or in connection with it. You must not provide this document or any information contained in it to any third party without our prior consent.

© Copyright, 2025. Smart Power Utilities Ltd ABN 72 121 464 864